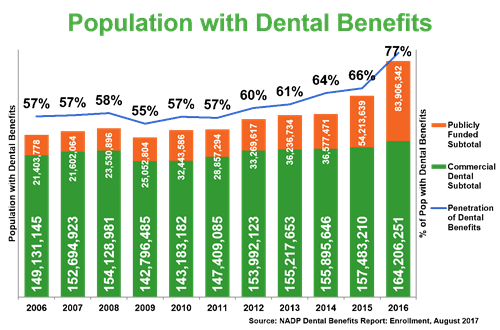

Do you understand how your dental insurance coverage works? In this article we will explain the important concepts and common questions many patients have about dental insurance. According to the 2017 NADP Dental Benefits Report, two-thirds of Americans have private dental coverage. December is usually a very busy time for many dentist offices (including our Lansdowne VA office) because many patients want to use their benefits before the benefit period ends.

Is Dental Insurance Truly “Insurance”?

Most dental insurance plans are not like auto or home insurance plans in the sense that they do not cover you for catastrophic and undesired occurrences. Take auto insurance for example, it will kick in only when you have accidents that have a low chance of happening. Auto insurance does not cover your car for a 6-month check-up so to speak, unlike dental insurance. Basically, most dental insurance plans are defined benefit plans with limitations. The limitations are there to contain their cost. As a patient, it is very important to know your plan’s limitations. Oftentimes the limitations are buried under small prints.

Key Concepts and Terms

Frequency limitations: Each plan has frequency limitations such as two cleanings per plan year. It is important to know what “plan year” means for your plan and if there are other fine lines. Most plans have a calendar year as their “plan year” while other plans have Mar. 1, June 1, Oct. 1, or Dec. 25 as the plan year’s start day.

Annual deductible: This is what the patient has to pay BEFORE your plan starts to pay the defined proportion of coverage. It renews every plan year. For many preventive services such as exam, cleaning, or x-ray images, the deductible is waived. You pay your deductible to your dentist but the deductible is charged by your dental plan not by your dentist.

Annual maximum: Each plan has predefined annual maximum. The plan will not pay anymore (penny more 🙂 ) when the total accumulated payment exceeds the annual maximum. Remember this is the TOTAL payment your plan has paid so far. It starts to pay again only after the new plan year starts.

Pre-authorization/pre-determination: Before you receive more extensive dental treatments such as deep cleaning, crown and bridges, dentures, and implants, your benefit plan wants to authorize it. Your dentist’s office sends all the necessary documents to the plan administrator (Aetna, Cigna, Delta Dental…) and they review it then send their statement explaining in detail how much they would “likely” pay. This is the best assurance the dentist and the patient can receive BEFORE the desired treatment. Unfortunately, there are NO GUARANTEES. The benefit plan can decide not to pay after the treatment is rendered based on the circumstances at the time of reviewing the claim.

This process typically takes 2-3 weeks and could be longer if the treatment is more extensive. Your benefit administrator is typically a huge company working on your case and it is hard to keep track of the progress. So please do not wait until the end of December to use your dental plan and FSA to receive big treatments.

Your patient payment portion: Your patient payment portion depends on many different factors as exemplified above. You would pay your estimated patient portion on the day of service but it may need to be adjusted based on what your dental plan decides on the proportion of payment.

Tips for Choosing the Right Dental Insurance Plan

Selecting the right dental insurance plan can be challenging. With so many options available, it can be difficult to know which plan is best for you and your family. Here are some tips for choosing the right dental insurance plan:

- Determine Your Needs – Consider your family’s dental needs when selecting a plan. Do you have children who need braces or regular check-ups? Are you or your family members prone to dental issues? Understanding your needs can help you select a plan that provides the coverage you need.

- Review Your Options – Research different dental insurance plans and compare their coverage and costs. Consider the frequency limitations, annual deductibles, annual maximums, and any pre-authorization requirements.

- Check Provider Networks – Ensure that your preferred dental provider is in-network with the plan you are considering. This can help you avoid out-of-pocket costs for seeing an out-of-network provider.

- Understand Your Costs – In addition to monthly premiums, consider any out-of-pocket costs, such as deductibles, co-payments, and coinsurance. Make sure you understand your estimated patient portion before undergoing any treatment.

- Read the Fine Print – Review your plan’s policy carefully, including the terms and conditions, to understand any limitations and exclusions. Be sure to ask your insurance provider or dental office staff any questions you may have.

We Are Here to Help

As your trusted Ashburn VA dentist (also serving Lansdowne VA and Leesburg VA), we are here to help you navigate the complicated world of dental insurance. We understand that selecting the right dental insurance plan can be overwhelming. Our team is happy to help you understand your options and select a plan that best meets your needs and budget. We accept a variety of dental insurance plans and will work with you to maximize your benefits and minimize your out-of-pocket costs.

In addition to traditional dental insurance plans, we also accept flexible spending accounts (FSAs) and health savings accounts (HSAs). These accounts can help you save money on dental care by allowing you to set aside pre-tax dollars for dental expenses.

If you have questions about dental insurance or need help selecting a plan, please don’t hesitate to contact us. Our team is here to help you achieve optimal oral health and a brighter smile.

About Dental Innovations of Virginia – Your Ashburn VA Dentist

Dental Innovations of Virginia provides comprehensive dental services, and preventive dentistry for the whole family. In addition to our Lansdowne office serving the Leesburg, Lansdowne, Ashburn and nearby areas, we also come to you via our DIVA Mobile Clinic service for patients living in long-term care facilities, and our DIVA Mobile Home Visit service for patients who prefer to receive treatments in the comfort of their own home.

Dr. Joon Coe, Dr. Julie Coe, and the rest of the DIVA team look forward to helping you achieve a brighter smile and the highest possible dental health. We’re located at 19490 Sandridge Way, Suite 160, Lansdowne, VA 20176. We’re open Monday through Friday from 9 a.m. to 6 p.m. Contact us to schedule an appointment or ask us a question.